Buying property in Florida looks simple on the surface — you find a listing, make an offer, and close the deal. What most first-time buyers discover too late is that the purchase price is only one part of what you actually pay. The costs that appear before, during, and after closing can add 10% to 20% on top of the listed price, and they don’t announce themselves in advance.

Most people think property decisions come down to price and location. In reality, it’s the ongoing and upfront costs that most buyers never calculated that create long-term financial stress. Knowing what those costs are before you make an offer is the difference between a smart purchase and an expensive lesson.

What are closing costs in Florida — and how much should you budget?

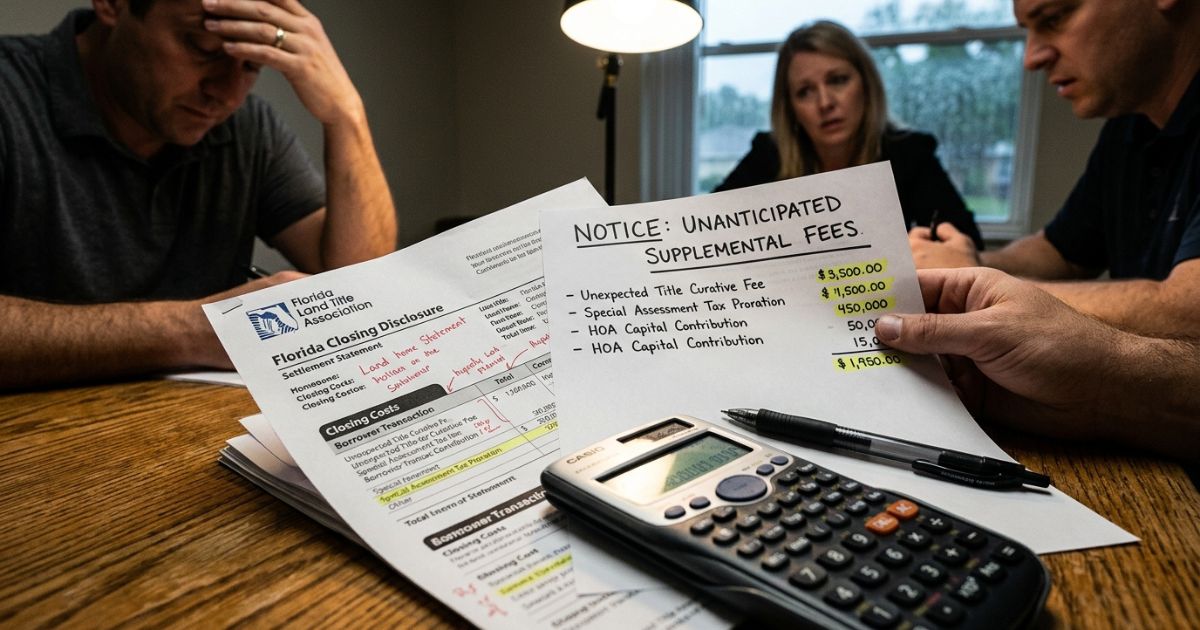

Closing costs are fees and taxes paid at the moment a real estate transaction is finalized. They’re not optional and they’re not included in the listing price. For buyers in Florida, closing costs typically fall between 2% and 5% of the purchase price — meaning on a $350,000 property, you should expect to bring an additional $7,000 to $17,500 to the closing table.

These costs generally include:

- Title insurance — protects against defects in the property’s ownership history

- Title search fee — a records search to verify the chain of ownership

- Recording fee — the county charge for recording the new deed

- Documentary stamp tax — Florida’s state transfer tax on real property

- Lender fees — if you’re financing, expect origination fees, appraisal costs, and underwriting charges

- Attorney or closing agent fees — highly recommended, especially for first-time buyers

Short answer: Florida closing costs typically range from 2% to 5% of the purchase price. These funds must be available at closing, separate from your down payment — and they're non-negotiable.

How much does homeowners insurance cost in Florida — and why is it higher than most states?

Florida consistently ranks among the most expensive states in the country for homeowners insurance, and the gap has widened in recent years. Hurricanes, flooding, and the volume of claims from major storms have driven premiums well above national averages — a fact that surprises many buyers relocating from northern states.

There are two separate coverages most Florida property owners need to consider:

What does standard homeowners insurance cover in Florida?

A standard homeowners policy covers structural damage, theft, liability, and most weather-related events — but it does not cover flooding. Premiums vary significantly by county, construction type, distance from the coast, and the age of the roof. Buyers in inland counties like Polk, Highlands, or Lake typically pay less than those purchasing near Tampa Bay, Miami-Dade, or the Atlantic coast. Annual premiums commonly range from $3,000 to $8,000 for residential properties — and significantly higher in coastal zones.

Is flood insurance mandatory in Florida?

Flood insurance is a separate policy entirely, and whether it’s required depends on the property’s FEMA flood zone classification. Properties in high-risk zones (designated AE or VE on FEMA maps) require flood insurance when financed through most lenders. Even in moderate-risk zones, many buyers choose to carry it — and for good reason. Annual premiums through the National Flood Insurance Program (NFIP) average between $900 and $2,500, though properties in the highest-risk zones can pay considerably more.

| Coverage Type | Required? | Typical Annual Cost |

|---|---|---|

| Homeowners Insurance | Required by lenders | $3,000 – $8,000+ |

| Flood Insurance (NFIP) | Mandatory in high-risk zones | $900 – $2,500+ |

| Wind / Hurricane Rider | Recommended in coastal areas | Varies — often separate deductible |

How does Florida property tax work — and what do first-time buyers actually pay?

Florida’s property tax is an annual charge assessed by each county based on the property’s appraised value. The effective tax rate varies by county but generally falls between 0.8% and 2% of assessed value per year. On a $400,000 home in Orange County, that translates to roughly $5,000 to $7,000 per year — a recurring cost that never goes away and should be factored into every budget calculation.

What is the Florida homestead exemption and do you qualify?

The homestead exemption is one of Florida’s most valuable tax benefits — and one of the most commonly misunderstood by first-time buyers. Florida residents who use the property as their primary residence can reduce the taxable value of their home by up to $50,000, significantly lowering the annual property tax bill. The exemption also includes a Save Our Homes cap that limits how much the assessed value can increase year over year.

However, this benefit only applies to primary residents. Investment properties, vacation homes, and properties owned by non-residents do not qualify — meaning many buyers coming from out of state or from another country pay the full, uncapped rate.

Short answer: Florida property taxes run roughly 1% to 2% of assessed value per year. The homestead exemption can reduce that meaningfully — but only if the property is your primary Florida residence.

What are HOA fees and CDD fees — and why do they catch buyers off guard?

How much do HOA fees cost in Florida communities?

A Homeowners Association (HOA) manages shared spaces and enforces community rules in planned neighborhoods and condominiums. Monthly fees range from as little as $100 in smaller communities to over $1,000 in luxury developments. Beyond the regular fee, HOAs can issue special assessments — unscheduled charges to fund repairs, infrastructure upgrades, or emergency expenses. These assessments are unpredictable, and some buyers have received bills for $5,000 or more with minimal notice.

What is a CDD fee and how does it affect your property tax bill?

A Community Development District (CDD) is a government-authorized entity created to finance the infrastructure of new developments — roads, water systems, parks, and streetlights. Unlike HOA fees, CDD charges are typically embedded in the annual property tax bill and are not optional. Many buyers purchasing in newer master-planned communities in counties like Osceola, St. Johns, or Pasco encounter CDD fees for the first time only after closing. They can add $1,000 to $3,000 or more per year to the effective carrying cost of the property.

What hidden costs should you expect when buying vacant land in Florida?

Vacant land purchases come with their own set of expenses that most buyers don’t anticipate. The sticker price on a parcel in central Florida might look attractive — but the cost to make that land usable is a separate calculation entirely.

- Land survey — required to confirm legal boundaries and property dimensions. Typically $500 to $2,000 depending on size and terrain

- Soil and percolation testing — necessary to evaluate septic viability and construction feasibility. Cost: $300 to $800

- Utility connections — connecting a raw parcel to electricity, water, and sewer can cost anywhere from $5,000 to $30,000 or more depending on how far the utilities are from the property line

- Zoning and deed restriction review — verifying that the land can be used as intended before purchase is critical. Rezoning after the fact is expensive, slow, and not guaranteed

- Building permits — permit fees vary by county and project scope, and the permitting timeline adds months to any development plan

What most first-time buyers get wrong about Florida property costs

- Not budgeting for closing costs separately — the cash for closing must be ready at settlement, in addition to the down payment

- Skipping the insurance research until after making an offer — insurance costs in some areas make certain properties financially impractical, and this is only discovered too late

- Assuming HOA and CDD information will be volunteered — always ask directly, in writing, before submitting an offer

- Buying vacant land without confirming utility access — a parcel without road access or utility infrastructure is not “ready to build,” regardless of how it’s listed

- Not calculating the total annual carrying cost — property tax + insurance + HOA/CDD fees + maintenance should all factor into affordability, not just the mortgage payment

What to verify before closing on a Florida property

- Request the full title report and confirm there are no outstanding liens on the property

- Look up the property’s FEMA flood zone designation at msc.fema.gov before budgeting for insurance

- Check the current assessed value and property tax bill at the county property appraiser’s website

- Ask your agent or the seller for documentation of all HOA fees, special assessments, and CDD charges

- For vacant land: confirm the zoning code with the county planning department and verify utility availability

- Hire an independent licensed home inspector — don’t rely solely on seller disclosures

Glossary

Closing costs — Fees and taxes paid at the time of closing a real estate transaction, typically 2%–5% of the purchase price. Separate from the down payment.

Title insurance — A one-time policy that protects the buyer against historical claims, liens, or errors in the property’s ownership record.

Property tax — An annual county-assessed tax based on the appraised value of the property. The effective rate varies by county.

Homestead exemption — A Florida tax benefit that reduces the taxable value of a primary residence by up to $50,000. Not available for investment properties or non-primary residences.

HOA (Homeowners Association) — A private organization that manages shared amenities in a community and charges monthly or annual fees to property owners.

CDD (Community Development District) — A government entity that finances community infrastructure through charges embedded in the annual property tax bill.

FEMA flood maps — Federal maps that classify properties by flood risk level. They determine flood insurance requirements and pricing.

Special assessment — An unscheduled charge issued by an HOA or CDD to cover unexpected expenses. Not predictable and can be substantial.

Lien — A legal claim or debt attached to a property that carries over to the new owner if not resolved before closing.

Land survey — A professional measurement of a property’s legal boundaries, size, and physical characteristics.

Immediate actions — Start now

- Calculate estimated closing costs (2%–5% of target price) and confirm those funds are liquid and separate from your down payment

- Look up the property’s flood zone classification at msc.fema.gov before budgeting

- Search the county property appraiser’s website for the current assessed value and annual tax bill

- Ask your real estate agent for written confirmation of any HOA fees, special assessments, or CDD charges

- Get at least two homeowners insurance quotes before submitting an offer — not after

- For vacant land: call the county planning department to confirm zoning and utility availability

- Hire an independent home inspector regardless of the property’s apparent condition

Conclusion

Florida remains one of the most attractive real estate markets in the United States — no state income tax, strong demand, and a wide range of property types for every type of buyer. But the listing price is the beginning of the financial conversation, not the end of it. Property taxes, insurance costs, closing fees, HOA charges, and CDD assessments are real, recurring, and significant.

Every one of these costs is verifiable before you make an offer. Buyers who ask the right questions early walk into closing with no surprises — and that’s what separates a well-planned purchase from an expensive mistake.

TerraNoble provides bilingual guidance in English and Portuguese for buyers navigating the Florida real estate market. Whether you’re purchasing a home, a vacation property, or vacant land, our team helps you understand the full picture before you commit. Reach out for a no-obligation conversation about your goals.